While everyone's focused on the Trump-Iran crisis, they're missing one of the most important turning points in the history of technology. Just days before this latest wave of geopolitical chaos, Nvidia‘s earnings quietly confirmed the start of a new phase of the AI revolution. Yes, the world is crazy right now. Yes, stocks could absolutely collapse in the short term. But that's exactly where millionaires get made, especially if you can be greedy when others are fearful without getting distracted. Your time is valuable, so let's get right into it. In a world where everyone's focused on the latest headlines and panic trades around every dip, the real winners will always be the investors who are ready for this moment ahead of time.

Table of Contents

1. NVIDIA’s Unprecedented Growth Surge

2. Projecting $78 Billion: Growth Without China

3. AI Agents Today vs. Tomorrow

4. Key Takeaways

The ones who trust facts over feelings and actually understand the science behind the stocks. I want to make the best use of your time with this video. And to do that, we have to focus on the long-term signals that actually matter for investors. So here's how I've organized this video. What Nvidia's latest earnings call actually means for the AI revolution, how AI agents are taking over the future of digital infrastructure right now, the massive impact this will have on Nvidia's long-term valuation and every other stock in the AI ecosystem, and of course, my new price target for Nvidia stock as a result. There's a ton to talk about, so let's dive right into their latest earnings.

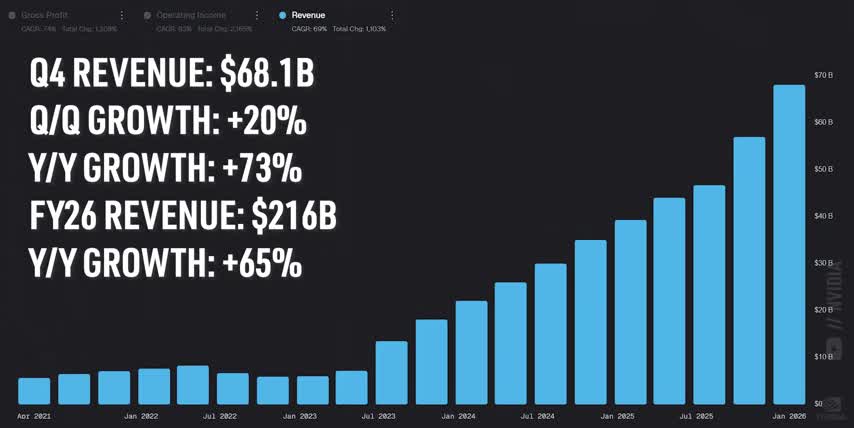

NVIDIA reported record revenues of $68.1 billion for the quarter, which is up 20% quarter over quarter and 73% year over year. They made $216 billion in revenue for the full fiscal year, which is a 65% increase from the year before. Earnings per share came in at $4.90 for the year, with $1.76 of that from just this past quarter. That's up 98% year over year. At this rate, I expect their earnings per share to more than double again by the end of 2026, to around $11 per share for the year and about $3.60 per quarter. Just think about these numbers for a second. The biggest company on earth is still growing revenues and earnings by over 70% per year. When's the last time the market saw so much growth at such a massive scale? But Nvidia's revenues aren't just growing.

They're actually accelerating as Blackwell Ultra production continues to ramp. Year-over-year revenue growth was 55% in Q2, 62% in Q3, and now 73% in Q4. Just like I said would happen after Nvidia GTC last year. But top-line revenue and earnings only tell half the story. And to really understand Nvidia's growth, we need to look at where it's coming from and how profitable it is. Gross margins came in at 75% for the quarter, with operating margins over 60%. That makes NVIDIA one of the most profitable semiconductor companies ever. In fact, they're as profitable as most market-leading software companies, except without all the risk of being disrupted by AI agents. That's a joke. Well, kind of.

Most of that profitability comes from their data center segment, which hit $62.3 billion in revenue this past quarter. That's up 22% quarter over quarter and 75% year over year. Datacenter now accounts for over 91% of Nvidia's total revenues. But here's where things get interesting. Within that segment, networking revenues came in at $31 billion for the year and $11 billion in quarter for a loan, an increase of 263% from a year ago. That insane growth is driven by NVLink, SpectrumX Ethernet, and InfiniBand. And that makes Nvidia the largest networking company in the world for AI data centers and high-performance computing. Networking isn't just a side business. It's a great way for Nvidia to diversify their offerings beyond GPUs.

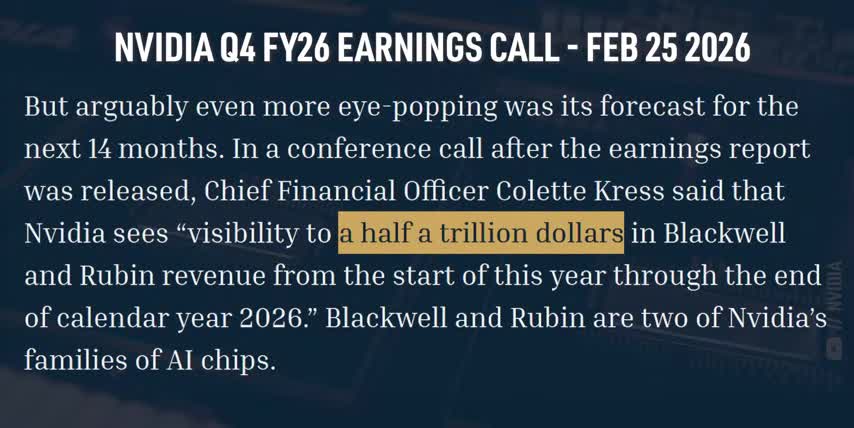

Every hyperscaler still needs huge amounts of high-speed, low-latency interconnects even when they deploy their own custom AI chips. That means Google Cloud, Amazon Web Services, and Microsoft Azure can build clusters around Nvidia's networking stack even when some of their compute comes from TPUs or in-house ASICs. My point is, networking doesn't just increase NVIDIA's revenues. It extends their reach across the entire AI data center landscape. That's why NVIDIA's CFO, Colette Kress, said they now have visibility into over half a trillion dollars of Blackwell and Rubin revenues through 2027 That their real revenue pipeline not some hypothetical demand And that pipeline is turning into huge cash flows Nvidia generated $35 billion in free cash flows just this past quarter, with over $96 billion for the full year.

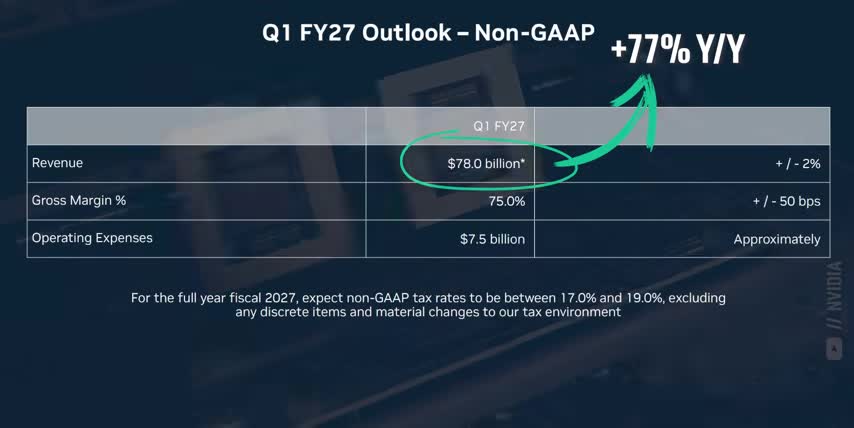

They returned over $40 billion to shareholders through share buybacks and dividends, with another $58 billion still authorized. And for next quarter, NVIDIA is projecting around $78 billion in revenues. That would imply 77% year-over-year growth from an already massive base. And that guidance still assumes zero data center sales to China, which means it doesn't depend on export approvals or tariffs. That also means that any sales to China would effectively be pure upside for the stock. On the earnings call, Jensen Huang boiled NVIDIA's entire quarter down into a single sentence.

Compute equals revenue, that's the inflection point we're at right now, where AI systems, applications, and even entire digital workforces directly turn compute into income, and that's exactly why Nvidia's revenues, profit margins, and cash flows are all accelerating as agentic AI systems start to scale in almost every market.

But there's something else on the market that you need to know about, and that's your private data, there are hundreds of online data brokers making big money by collecting and selling your personal information, that's why I've been using this video's sponsor, Delete Me, for over two years now, and I really can't recommend them enough.

Delete Me is a hands-free subscription service that will remove your personal information from those online data brokers, they give you a quarterly privacy report showing everything they've done, and they've reviewed over 55,000 listings for me so far, but what really surprised me is these data brokers had way more than just my private data, they had my wife's and my entire family's too.

That's another reason I really like Delete Me, they have a family plan, so we can all have more control over our personal data, so if you care about your data and your family's privacy, you can get 20% off any consumer plan with my code “symbol20” by going to join Delete Me dot com slash symbol20, or by using my link in the description, and a big thank you to Delete Me and to you for supporting the channel.

All right, and Nvidia's earnings are really just the scorecard for the AI revolution.

Their revenues, margins, and cash flows are accelerating because demand for AI processing is accelerating. And like Jensen said on the earnings call, compute equals revenue. Not because more people are typing more prompts into more chatbots. That can't scale forever. This acceleration is all about AI agents. Tools like Claude Cowork, OpenClaw, and Perplexity Computer aren't just answering questions. They're doing work, creating and coordinating with other agents, moving money, and running almost non-stop in the background. It took me a long time to understand the economics around AI agents, but I've finally wrapped my head around it. So let me tell you something that will put you ahead of almost every Wall Street analyst trying to cover this area of AI.

First, these agents are not going to replace most jobs. They'll either support the people doing them, or they'll do the work that most companies would never pay a human to do in the first place. Think about boring, low-value and continuous work, like manual data entry, standardizing thousands of documents, monitoring internal systems, or answering frequently asked questions. So, it's better to think of AI agents more like a utility, like the internet, electricity, or gas. We measure AI in terms of tokens, and the goal is to spend those tokens to do something productive, just like we use the internet, electricity, and gas to create value once you look at it that way the returns on ai start to make a lot more sense let me show you what i mean when a company hires someone they usually aim for at least a 2x return on that person's total cost including their salary benefits training their computer and so on so if somebody costs a hundred thousand dollars a year after everything the company wants to make at least two hundred thousand dollars of value from their work so that person has a 50 profit margin.

Now let's give them access to an AI agent. The top tier plans for tools like Claude Cowork or Perplexity Computer cost roughly $2,000 per user per year.

But let's be generous and double that to cover all the enterprise extras like higher limits, security, admin controls, and so on.

Let's say an AI agent makes that person just 50 more productive by doing only the most obvious things that we all know AI can do today, basic research, formatting emails and reports, taking notes in meetings, answering basic questions about articles we all pretend to read, and making rough first drafts of documents and code.

Most studies show much higher productivity gains, especially when it comes to coding and writing, but we're being ultra-conservative here.

So now, with an AI agent, that same employee costs a hundred and four thousand dollars a year, but generates three hundred thousand dollars worth of value, instead of two.

Their profit margin jumps from 50 percent to 65 percent, or said another way, the company made an extra one hundred thousand dollars for a four thousand dollar investment, and that's assuming the AI agent can only help one person, nothing says these systems can't support two people or five or an entire team.

Charlie Munger famously said, “Show me the incentives and I'll show you the outcome,” well, when the incentive is a 10, 20, or even 30x return per AI agent, the outcome is crystal clear.

Any company not investing in AI will eventually get out competed by one that is, but here's what most investors haven't really realized yet, these AI agents are now working with tools and other agents to push those productivity gains even further.

AI models are building skills, using shells, and they're able to run longer workflows autonomously. Skills are basically reusable tools, like using APIs, updating spreadsheets, filing tickets, and committing code. Shell access lets agents run commands, install packages, call other programs, and manage files in computers, not just inside their own chat windows.

And workflow engines let them chain these skills and tools together, so one agent can research while another one plans a third executes the plan and a fourth one can qa the result all running autonomously instead of relying on human prompts at every step.

Another thing investors may not realize is that the web itself is becoming more agent friendly, more websites and APIs are creating machine readable endpoints, structures, markdown files, and protocols that let agents find things and call each other directly, so instead of pages designed for human readability, we're starting to see content structured specifically for parsing, reasoning, and chaining into the next action.

Now put that all together, one agent calls a skill to fetch some data, another agent takes that output, runs an analysis in a shell, writes its own files, and calls a third agent to push changes into a test environment, then another agent tests the code and if something looks off, it can wake up a fourth agent to roll back those changes or open a ticket for a human to resolve the issue.

This is a huge shift in how people and AI's work together, instead of short bursts of back and forth chats, people are kicking off long-running, multi-step inference jobs with lots of tool calls, shell usage, and agent to agent communications, that means more tokens per task, more context held in memory, more bandwidth across the network, and more jobs running at once, or said another way, more compute equals more revenue.

And now we've come full circle, because more complex, longer-running, multi-agent workflows directly lead to more demand for Nvidia's systems, and with all that context, we can talk about my predictions and price target for Nvidia stock, and if you feel I've earned it, consider hitting the like button and subscribing to the channel, that really helps me out, and it lets me know to make more content like this, thanks.

Now let's talk about my price target for Nvidia stock, my price target for Nvidia stock is 411 dollars per share, which implies a 10 trillion dollar valuation, which is about 130% upside from here.

It won't get there tomorrow, it won't get there next month, and it probably won't get there next year. But I genuinely believe it'll happen much sooner than Wall Street thinks, and it will obviously bring many other AI infrastructure companies along for the ride. Here's how I think it happens. NVIDIA won't hit a 10 trillion dollar valuation because of hype, but for the exact opposite reason. AI agents will become boring but critical infrastructure, just like the enterprise software systems we already rely on today.

Today, almost nothing is run by AI agents end to end, and the average person uses AI to help them research write or code Most AI tools are basically auto with a few built actions like web browsing uploading files and automations to summarize meetings and draft emails Almost all of our digital infrastructure still runs on traditional software. Marketing and sales systems, payment processors, logistics platforms, cybersecurity tools, higher-level customer support, the list goes on and on. Sure, there are some AI agents running in the background to do things like watching logs, handling low-level tickets, and scraping data, but they're basically automated helpers bolted onto existing systems. I think that balance will shift over the next few years.

Agentic platforms will build entire libraries of complex skills. They'll learn to interface with virtually every digital tool, and they'll run for much longer without interruption. Just like we expect self-driving cars to eventually take full responsibility for every step of driving, from planning and pickup, to navigation and accounting for traffic, to drop-off and self-parking, there will be a point where digital agents take full responsibility for monitoring, deciding, and executing end-to-end processes, instead of asking for instructions at every step.

Websites and enterprise systems are already being wired up with machine-readable interfaces and agent-focused APIs, so they can talk directly to customer databases like Salesforce, finance and accounting platforms like NetSuite and SAP, payment systems like Stripe and Visa, e-commerce platforms like Amazon and Shopify, ticketing tools like Zendesk and ServiceNow, cloud dashboards like AWS and Azure, and all the internal tools that companies use to manage their work today. As that trend continues, more of our digital infrastructure will start being handled by agents that run 24-7, and only escalate things to humans when there's an issue. And that's just for the systems we already have today.

The next wave of systems, which haven't even been built yet, will be designed from the ground up with agents in mind, where the default assumption is that AI clicks the buttons and moves the data, while humans set the goals and the requirements. All of this translates into far more tokens per user and per workflow, especially as agents become users themselves.

Every extra step, tool call and agent to agent message means we need more network bandwidth, more context held in memory and more compute, which is exactly what turns into more revenue for Nvidia.

Nvidia's data center revenues are already over 62 billion dollars a quarter, a 10 trillion dollar Nvidia would probably have on the order of 110 billion dollars in quarterly revenues or roughly 450 billion a year, which means their data center business has to double again from here.

That assumes their gaming, professional visualization, automotive and physical ai segments don't add any meaningful upsides of their own, that sounds like a huge leap, but nvidia is already growing revenues at 73 percent year over year and they're guiding for 78 billion dollars in revenue next quarter, which implies a 77 growth rate.

And that guidance assumes zero data center revenues from china, nvidia obviously can't grow at this rate forever, but really they don't have to, even if growth got cut in half to roughly 35 per year, they'd still reach 400 billion dollars in annual revenues by the end of the decade.

But on top of that, nvidia also has to defend their current 75 gross margins and 60 operating margins, numbers that make them look more like a top-tier software company than one designing semiconductors, if ai agents keep getting more capable, more integrated and more central to how digital work gets done.

And if rivals don't eventually force Nvidia to compete on price, then a $10 trillion valuation is the logical conclusion for the company powering the entire agentic AI revolution.

Like I said at the start of this video, in a world where everyone is panicking over the latest headlines, the real winners are the investors who are always ready ahead of time. The ones who trust facts over feelings and actually understand the science behind the stocks. let me know what you think about my 411 price target for nvidia stock in the comments is a 10 trillion dollar valuation impossible or is it inevitable and if you want to see more science behind the stocks check out this video next either way thanks for watching and until next time this is ticker symbol you my name is alex reminding you that the best investment you can make is in you.

Key Takeaways

- Nvidia's latest earnings call confirmed the start of a new phase of the AI revolution.

- Ai agents are taking over the future of digital infrastructure, leading to increased demand for Nvidia's systems.

- The company's data center revenues are growing rapidly, with a 75% gross margin and 60% operating margin.

- Nvidia's valuation could reach $10 trillion, implying a 130% upside from current prices.

- The company's growth is driven by the increasing use of AI agents in various industries, leading to more compute and revenue.

Checkout our YouTube Channel

Get the latest videos and industry deep dives as we check out the science behind the stocks.