In less than a week, SpaceX will have engineered the biggest wealth transfer in stock market history, bending or rewriting every rule designed to protect investors from this exact scenario, and leaving retail investors holding the bag even if we don't actually buy SpaceX stock ourselves. My name is Alex, and I spent 8 years as an electrical engineer and AI researcher at MIT, 4 of them at the launch facility where SpaceX tested their Falcon 1 rockets. Let me show you what makes this IPO so dangerous for investors, and why I'm avoiding it. Your time is valuable, so let's get right into it. For as long as I can remember, I've been fascinated by the stars. To me, space is the ultimate and final frontier.

A universe filled with distant planets, alien civilizations, and endless wonders to explore. When I was younger, I applied to be an astronaut, and when I didn't make it, I became a rocket scientist instead. While I was at MIT's Lincoln Laboratory, I spent four years in the Marshall Islands as one of the lead radar engineers at the Ronald Reagan Space and Missile Test Range, the same place where SpaceX tested their early Falcon 1 rockets. I wasn't there for those tests, but I worked with many engineers, scientists, and technicians who were. And one thing we all had in common was a deep respect and admiration for the SpaceX mission, making humanity an interplanetary species. I suspect that many of you watching this video have that same deep respect and admiration.

Unfortunately, that's not the company that's about to go public. Let's start with the basics. When a company goes public, they file an S-1 form with the SEC, the Securities and Exchange Commission. This document discloses everything the market needs to know about the company, the business model and biggest risks, the financials, the ownership structure, and so on. SpaceX filed their S-1 form on May 20th, and it runs 277 pages. But the surprises start on page 1. Every company on the market is grouped into an industry, and every industry has a code. 3760 for space vehicles, 3812 for defense or aeronautical systems, 4522 for air transport. Companies like Boeing, Lockheed Martin, Raytheon, and Virgin Galactic all fall under these codes. But SpaceX filed under 7370.

computer programming, and data processing. The further into this S-1 form I got, the more I felt like this entire document was designed to trick me. It opens with 18 photographs of rocket launches and satellites, a quote from Elon Musk on making humanity a space-faring civilization, and the mission of extending the light of consciousness to the stars. Cargo runs to the moon, manufacturing on Mars, asteroid mining, it's all in there. But that's just the prologue. The real story begins on page 11, and it's not a space story at all. According to this S1 filing, SpaceX's total addressable market is $28.5 trillion, which is roughly the size of the entire US economy. It breaks that market into three segments, space, connectivity, and AI.

Space Market

And it turns out that space is only $370 billion of that market, 1.3%. Even Starlink, which connects all of humanity together and to the internet, is just 1.6 trillion. 93% of SpaceX's total addressable market is AI, and most of that falls under standard enterprise applications, the kind that Anthropic, OpenAI, and Google already dominate. Investors are excited to own a piece of humanity's future among the stars. But for every dollar SpaceX gets, only a penny leaves Earth's orbit. I want to respect your time, so let's cover the other 99 cents first. Just a few months ago, SpaceX acquired XAI in an all-stock deal. If you didn't know, XAI is the AI company Elon Musk started in 2023, to compete directly with OpenAI and Anthropic.

XAI's flagship product is Grok, an AI chatbot integrated directly into X, the social media platform formerly known as Twitter. In a report published last year by Netscope, which tracks how thousands of corporate customers connect to AI models, Grok failed to gain any significant traction in corporate environments. Just two out of every 1,000 enterprise users use GroK, and those that do, spend less than half the time with it than they do with ChatGPT. Even SpaceX's filing acknowledges that the AI market is dominated by ChatGPT, Claude, and Gemini. Last year, XAI launched an image editing feature for GroK.

XAI Product

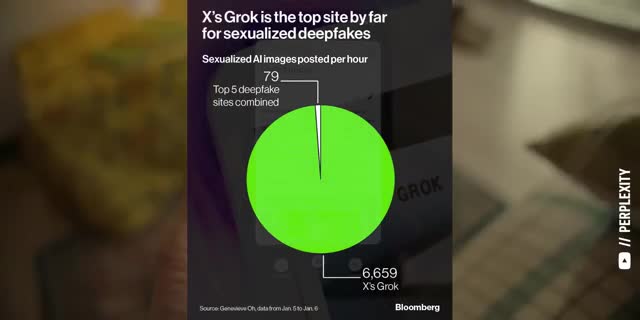

In an 11-day window between December 29th, 2025 and January 9th, 2026, users generated over 4 million explicit and non-consensual images of real people, including an estimated 23,000 pictures of minors. Researchers calculated that at its peak, Grok was producing 6,700 of these illicit images every hour, 84 times more than the top five deepfake websites combined. There are multiple ongoing regulatory actions and active lawsuits around this incident. SpaceX's S1 form explicitly lists these investigations as a risk factor and sets aside $530 million in part to cover these claims Elon Musk co XAI with 11 other AI researchers All 11 of them have since left the company and Elon Musk himself has said that the AI needed to be rebuilt from the ground up on March 12th of this year, less than 90 days ago.

That's the product that SpaceX paid $250 billion to acquire. That's the product that represents 93% of SpaceX's total addressable market. That's the product you're actually investing in when you buy SpaceX stock. Look, I'm always traveling to AI conferences to interview industry leaders, research products and prototypes, and hunt for new investments. That means I'm constantly connecting to random Wi-Fi networks at airports, hotels, cafes, and convention centers. That's why I use Surfshark, the sponsor of this video. Surfshark protects my data by encrypting it and changing my digital location. That makes my online activity much harder to track, even on sketchy public networks.

Surfshark

Surfshark is super fast, easy to use, and I can install it on unlimited devices with just one account, to protect myself and my entire family. Also, it actually saves me money. Many online stores raise their prices based on your location. So I use Surfshark to always get the best price on big purchases like plane tickets, hotel rooms, and rental cars. And third, Surfshark also lets me access content, websites and services that are blocked in my location, all for less than $1 a week. Talk about a no-brainer. So if you want to protect your family's data and you like saving money, go to surfshark.com slash ticker to start your 7-day free trial and get up to 4 extra months for free. And with Surfshark's 30-day money-back guarantee, there's no risk in trying it with my link below today.

Alright, so if Grok makes more trouble than revenue, how does SpaceX's AI segment actually make its money. It rents out GPUs. Anthropic agreed to pay SpaceX $15 billion a year through May of 2029 for access to all 220,000 NVIDIA GPUs from XAI's Colossus One Data Center in Memphis, which represents about 40% of SpaceX's near-term AI revenue. But here's the part that didn't make the headlines. Colossus One was built with a mix of different NVIDIA GPU generations, – mainly Hopper H100s, H200s, and Grace Blackwell chips. When you try to train a Frontier AI model on a mix of GPUs, the faster chips spend most of their time waiting for the slower ones. An independent analysis found that Colossus 1 ran at just 11% of its max compute capacity during training.

Colossus One

And XAI had to move Grok's training workloads to Colossus 2. So now, SpaceX is stuck renting those mixed GPU clusters to their biggest competitor in the AI space. Adanthropic can cancel this deal at any time on 90 days notice. Here's another fun fact from the S1 filing. SpaceX spent $506 million on Tesla Megapack batteries and another $131 million on Cybertrucks, which works out to over 1,200 trucks. SpaceX paid full sticker price for all of them. No volume discount. No friends and family pricing. Nothing. At one point late last year, SpaceX accounted for 18% of all US Cybertruck registrations. So Elon's companies aren't just buying each other, they're also buying products from each other at full sticker price using shareholder money.

Speaking of shareholders, it's essential to understand exactly who owns SpaceX shares today, since that's who's selling them when the company goes public. Back in 2022, Elon Musk raised $44 billion to buy Twitter. Within a year, the company was worth less than half of what he paid, which means the banks and investors who helped finance the deal were sitting on billions of dollars in losses. The fix was pretty simple. AI was everywhere, and Elon owned an AI company. So in 2024, he merged X into XAI. No cash changed hands, and Twitter's losses became an equity stake in a cutting-edge AI company. But that created a new problem. XAI was burning over a billion dollars a month with no path to profitability and a product that had to be rebuilt from scratch.

So, in February of this year, SpaceX acquired XAI. No cash changed hands, and XAI's losses became an equity stake in a cutting-edge space company. Everyone who helped Elon Musk buy Twitter in 2022, Andreessen Horowitz, multiple investors from Saudi Arabia, and even Twitter's founder Jack Dorsey himself, is now holding SpaceX shares, just in time for the largest IPO in stock market history. I spent a lot of time on XAI because it accounts for 93% of SpaceX's total addressable market, at least for the near term. So now let's talk about the other 7%. Before SpaceX, it cost $54,000 to put one kilogram in orbit with the Space Shuttle. SpaceX does it for under 3,000.

SpaceX Cost

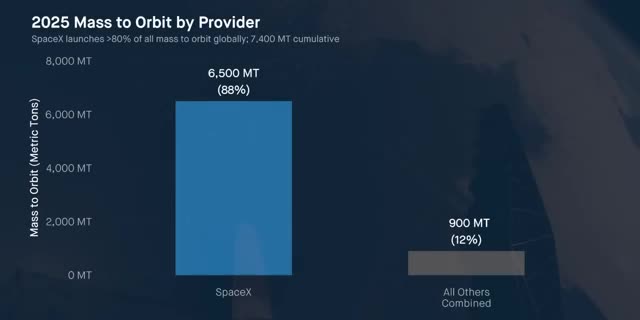

That's because the Falcon 9 booster lands itself on a drone ship, gets refurbished, and can fly again, drastically reducing overall launch costs. SpaceX's record is 34 flights on a single booster As a result SpaceX launches more than 80 of all mass that goes into orbit right now 165 missions last year alone which is more than half of every rocket launch on Earth As a space nerd I think that genuinely awesome According to SpaceX S1 filing, the rocket business generated $4.1 billion in revenue in 2025, and it spent $4.8 billion running it, which results in a $657 million operating loss. As an investor, not so awesome, especially when you consider that this rocket business is 24 years old. That operating loss is mostly due to Starship.

Starship actually accounts for just 14% of SpaceX's total capex, even though getting it to work at scale is a massive part of the $1.75 trillion valuation. In 2017, SpaceX's president, Gwen Shotwell, stood on a TED Talk stage and said that Starship would let you fly from New York to Shanghai in 39 minutes for the price of an economy class ticket. Travel between any two cities on Earth in under an hour. It's 10 years later, and Starship's 12th test flight just launched on May 22nd. The upper stage splashed down safely in the Indian Ocean. The booster crashed in the Gulf of Mexico. The FAA declared it a mishap and grounded Starship pending an investigation. There are no regulations for flying passengers over populated cities by rocket.

No airline, no airport, and no government has signed on. And SpaceX's own S1 has no timeline for when any of this will become a reality, let alone a service worth investing in. But one service actually worth investing in is Starlink, the crown jewel of the entire company. Starlink generated $11.4 billion in revenue last year, and $7.2 billion in adjusted operating profits. That's 61% of SpaceX's total revenue at 63% margins. So this is a real business today, and it's growing fast. Starlink had 2.3 million subscribers in 2023. By the end of last quarter, it had 10.3 million, up over 100% year over year. Starlink is active in over 100 countries, serving consumers, ships, airplanes, and even governments. It generated $3 billion in free cash flow last year alone.

Table of Contents

1. Space Market

2. XAI Product

3. Surfshark

4. Colossus One

5. SpaceX Cost

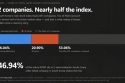

So SpaceX is almost 50% more expensive, growing almost two times slower, and has much lower margins.

Not to mention, it's not profitable while Palantir turned profitable last year.

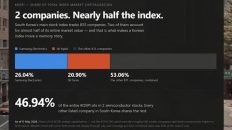

If SpaceX was in the S&P 500 today, it would be the seventh biggest company in the index, right between Meta Platforms and Tesla by revenue.

It's not even in the top 200, and that's just the beginning.

SpaceX has three classes of stock: Class A is what the public gets, which comes with one vote per share.

Class B is what Elon Musk and insiders get, to keep 10 votes per share.

There will actually also be Class C shares, but they haven't been issued yet, and they come with zero votes.

So, Elon Musk owns 42% of the shares, but controls 85% of the votes.

He's the company's CEO, CTO, and Chairman of the Board, that means the only person who can remove Elon Musk from any of those positions is Elon Musk.

But here's where things get interesting.

In January of this year, the SpaceX board granted Elon 1.3 billion performance shares At the IPO price of per share that billion These shares vest only if SpaceX stock hits specific market cap milestones and eventually only if they can establish a permanent human colony on Mars with at least 1 million people. That sounds great. Of course Elon should be rewarded for building the company that puts a million people on Mars. The problem is he doesn't actually have to do it. When performance-based milestones are classified as not probable, The rewards for those milestones can be booked at zero cost on the balance sheet. That makes sense since they're unlikely to happen. But according to the S1 filing, Elon can already vote these shares before they vest.

And he can already use them as collateral for personal loans. So for all intents and purposes, Elon gets a $175 billion payday with no market cap milestones hit, no colony on Mars, and no way for you to vote against it as a shareholder. even a corporate opportunity carve out in SpaceX's charter. Which means that Elon Musk and certain board members have no legal obligation to bring business opportunities to SpaceX first. They can take those opportunities to Tesla or any future venture and SpaceX shareholders can't do anything about it. You can't even sue and you literally waive your right to a trial by jury the moment you buy the stock. Your only right as a shareholder is to sell your shares. And even that is harder than it sounds because SpaceX is about to get added to the Nasdaq 100.

That's a big problem. Let me show you why. When you put money into an index fund, you're not picking stocks. You're letting the fund pick for you because you trust the rules that guide the fund's investments. The Nasdaq 100 is the second biggest index in America, only after the S&P 500.

It's trusted by pension funds, retirement planners, and passive investors of all sizes, from individuals all the way to institutions.

Nasdaq just changed two rules designed to protect all of these investors from this exact scenario.

First, they introduced a fast entry rule: any company big enough to rank in the top 40 by market cap can be added to the index just 15 trading days after going public.

A stock that just went public has no track record, the price is set by bankers and insiders, and it can take months of trading, earnings reports, and analyst coverage for the price to stabilize.

So, the Nasdaq made companies wait anywhere from 3 to 12 months before adding them to the index to protect investors from exactly that volatility, especially since stocks are notoriously overpriced when they first IPO.

This also stops investors from piling into the IPO just because they know that indexes will be forced to buy them, which drives the price up even more.

This new fast entry rule gets around all of those protections just in time for SpaceX's IPO.

Second, it eliminated the 10% minimum free float requirement.

SpaceX's float is only 4-5%. In English, that means only 4-5% of SpaceX's shares will be publicly tradable. The insiders controlling the other 95% can effectively set the price by choosing when and how much of their shares to sell. The 10% minimum free float requirement was designed to ensure that enough shares were in circulation so that no single shareholder could dominate the price. On top of that, most companies have a standard lockup period that stops insiders from selling their shares for 180 days. That way, they can't take advantage of the initial post-IPO run-up. But SpaceX insiders can sell up to 20% of their eligible shares right after the first earnings report. And if the stock price is up by 30% from the IPO, they can sell even more.

After that, new shares unlock every 15 days, until everything is already fully unlocked by the time the standard lockup period would have ended. And some insiders literally don't have to wait at all. SpaceX reserved 5% of their IPO shares for executives, friends, and family. For example, everyone who funded X and XAI over the years that got rolled into SpaceX stock. They could have zero lockup, which means that they can sell into a market where massive index funds are forced to buy the stock. index funds held by us. Forced to buy Twitter and Grok and all of the lawsuits and regulatory actions that come with them. Forced to buy the stock at an insane 94 times sales.

That makes SpaceX four times more expensive than Nvidia, which is the biggest company in the world by market cap, even though SpaceX is growing half as fast and from a much smaller revenue base. So that's why I'm not buying SpaceX stock. I'm also selling my shares of the Nasdaq 100 and buying VGT instead, Vanguard's Information Technology ETF, which I often cover on this channel. VGT consistently outperforms the triple Qs, it has lower management fees, and it tracks an index that won't include SpaceX. Honestly, we deserve better. And if you want to see what stocks I'm buying instead of SpaceX, check out this video next. Either way, thanks for watching, and until next time, this is Ticker Symbol You. My name is Alex, reminding you that the best investment you can make is in you.

Key Takeaways

SpaceX's IPO is a highly anticipated event, but it poses significant risks to investors due to its high valuation and lack of profitability. The company's S-1 filing reveals that 93% of its total addressable market is in AI, not space exploration. SpaceX's acquisition of XAI, an AI company founded by Elon Musk, is a significant factor in this valuation. However, XAI's product, Grok, has failed to gain significant traction in corporate environments, and the company is facing regulatory actions and lawsuits. SpaceX's financials show that the company is still losing money, with a $657 million operating loss in 2025. The company's valuation is 94 times revenue, making it one of the most expensive companies in the world. The Nasdaq 100's new fast entry rule and elimination of the 10% minimum free float requirement will allow SpaceX to be added to the index just 15 trading days after its IPO, which could lead to significant volatility and risks for investors.

Checkout our YouTube Channel

Get the latest videos and industry deep dives as we check out the science behind the stocks.