Mentioned in Video:

- 💰 Outperforming Cathie Wood?! My Portfolio Revealed: https://www.youtube.com/watch?v=hlHDXh3ymgk

- ⚠️ Cathie Wood: Warning to Banks & Which Companies Will Disrupt Them (ARK Invest Big Ideas 2021): https://www.youtube.com/watch?v=VV9YNg0eGVI

- 🌏 SE Stock | ARK Invest Has $550M in Sea Limited Stock: https://www.youtube.com/watch?v=czDuE7AoWHE

- Peak Fintech Investor Relations (TNT): https://peakfintechgroup.com/investors/

- ARK Invest's Whitepaper on Cash App (SQ) vs. Venmo (PYPL): https://ark-invest.com/white-papers/cash-app-vs-venmo/

- Peak Fintech Earnings Beats Estimates (first link is to the Zacks Report): https://finance.yahoo.com/news/pkkff-peak-fintech-beats-estimates-121600587.html

- Direct Download (PDF) Link to the Peak Fintech Zacks Report: https://s27.q4cdn.com/906368049/files/News/2021/Zacks_SCR_Research_09012021_PKKFF_Thompson.pdf

- Support the channel and get extra member-only benefits by joining us on Patreon: https://www.patreon.com/tickersymbolyou

🧨 One of my favorite #ARKInvest funds is #ARKF, #CathieWood‘s Fintech Innovation Fund. Let's take a look at a Canadian #Fintech company operating in China called #PeakFintech (TNT stock) and I'll show you why I think it's a perfect fit for @ARK Invest, even though they're out of most Chinese stocks right now. I used to hold Peak Fintech Group stock when it was PKKFF in my personal portfolio and plan on buying it again because I think TNT stock is about to explode!

Video Transcript:

00:00

The idea behind this channel is simple; connect the dots between ARK Invest's market research,

00:05

stock picks, and daily trading data to highlight the best investing opportunities among companies

00:09

that are transforming our daily lives. But what if we start applying some of the technology

00:14

and economic trends ARK Invest is always talking about to stocks outside their portfolios?

00:20

Can we find stocks that would make sense for Cathie Wood to hold in ARK Invest's funds

00:23

and buy them before she does? The answer is an obvious yes. One of the things every disruptive

00:29

company has in common is that they're using advanced technologies to solve modern problems

00:34

that legacy companies aren't doing a great job solving for one reason or another. So

00:38

one thing we can do is use ARK Invest's research to find these modern problems, pick the ones

00:44

with huge total addressible markets, and see who's solving them, regardless of whether

00:48

ARK Invest holds that company or even invests in that market. Here's a good example. 17

00:54

million people in the US are underbanked or completely unbanked. About 4 and a half

00:58

percent of those are small business owners, so that's about 765,000 small businesses.

01:04

Traditional banks can't really solve that problem because they have high customer acquisition

01:09

costs thanks to all of the physical assets they need to pay for; think big buildings

01:13

in the best parts of major cities, all the staff inside them, huge networks of ATM machines,

01:19

and so on. These big banks aren't willing to go after businesses they don't think they

01:23

can make a positive return on over time, which means they can't afford to serve many of the

01:28

businesses that are currently unbanked! Pretty ironic, right? Digital banking solutions don't

01:33

have those physical assets, which means they can make a positive return on a tiny business

01:39

much quicker. Those reduced customer acquisition costs let digital banks do 2 things: spend

01:44

some money poaching smaller businesses from big banks with better offers AND acquiring

01:49

underbanked businesses with less money in the first place, since they can still earn

01:53

a profit off of them while big banks can't. This big difference in customer acquisition

01:58

costs between big banks and digital wallets is something ARK Invest really hammers on

02:02

in their research on Square, Paypal, and other digital banking solutions found in ARKF, their

02:08

Fintech Innovation Fund. Well, it turns out that unbanked businesses are a fairly small

02:12

problem in the USA, because those 765,000 underbanked businesses account for less than

02:19

2 and a half percent of all small businesses in the US. Relatively speaking, it seems that

02:22

this is a fairly solved problem, right?

02:23

Well, if you zoom out to the rest of the world, you can see that this is actually a huge problem

02:27

pretty much everywhere else, which means the market opportunity is actually enormous. Around

02:33

two thirds of Latin America and the Middle East are underbanked or unbanked completely.

02:38

Around 60 percent of Southeast Asia is unbanked. According to a study done by Google, Bain,

02:43

and Sea Limited, that number could actually be as high as 75% percent in Southeast Asia.

02:48

In Sub-saharan Africa, the number is as high as 80% percent. No one company can solve this

02:52

MASSIVE problem worldwide because the financial culture of each region is different, as are

02:57

their banking systems and regulations. A one-size-fits-all Fintech solution just doesn't make sense,

03:03

so to fully capitalize on this world-wide opportunity we need to be picking the winners,

03:08

plural, that will emerge region by region. Even though ARK Invest is out of Chinese stocks

03:13

right now, the stock I want to talk about in this episode focuses on solving this problem

03:18

for small and medium sized businesses in China in a way that the Chinese government supports.

03:24

That's important to recognize in light of the recent regulatory crackdowns. The name

03:28

of the company is Peak Fintech Group and it just uplisted to the NASDAQ in early September

03:33

with the ticker symbol T N T, which is very fitting, giving how much the stock's price

03:38

has exploded over the last 3 months. I think Peak Fintech belongs in ARKF, since it uses

03:44

advanced technology to solve societal a problem ARK Invest cares about in a market where this

03:49

problem is massive. Full disclosure, I used to hold 8100 shares of this stock with an

03:54

average cost basis of $2.82 when it was still listed on the OTC Markets and I just sold

04:00

my last share at $10.00 even. So, I currently don't own this stock but will 100% be buying

04:05

back into it when I start my $100,000 public portfolio to compete with Cathie Wood's ARKK,

04:12

which I'll talk more about at the end of the episode.

04:15

Let's dive into Peak Fintech Group, starting with the problem they're solving. Over 100

04:20

MILLION small businesses in China had a hard time getting access to credit in the last

04:25

3 years. That's 130 times more than the US number I gave you earlier and is largely attributed

04:31

to the structure of China's financial system, which is fragmented and difficult to navigate.

04:36

The first part of solving this problem is bringing the data from all of these financial

04:40

fragments together and standardizing it to make apples-to-apples decisions about how

04:44

to connect businesses who need money with lenders who have money. That's what Peak Fintech

04:50

does; it's basically Tinder between businesses and banks. But uh, without all the swiping

04:55

and creepy messages. Nevermind. Lenders want to see bank statements, government approvals,

05:00

and so on from a business, while the business wants to understand the criteria they need

05:04

to meet to get approved for a loan. Once all this data from lenders, brokers, banks, businesses,

05:11

and other data providers is all in one place and standardized, Peak Fintech uses data analytics

05:16

and artificial intelligence to match lenders and vendors. If you've been watching my channel

05:21

for a little while, you'll know I'm obsessed with this idea of frictionless value transfer,

05:26

again, an idea that Cathie Wood and ARK Invest relentlessly focus on. The basic idea of frictionless

05:32

value transfer to take an inconvenient but necessary process – like getting a loan, going

05:37

to the doctor, talking to other people (ughgh) – and make it more convenient with technology.

05:44

Here's how Peak Fintech reduces friction for the participants in their ecosystem. For Small

05:48

and Medium-Sized Enterprises, it's free to sign up and you automatically get matched

05:53

with ALL the lenders you qualify for without needing to shop around, which is often the

05:58

most difficult part of getting a loan.

06:01

Peak Fintech reduces friction on the lender side by putting the right businesses who want

06:05

the right-sized loans right in front of them based on pre-established criteria. That means

06:10

businesses win 3 different ways: they don't need to spend as much money on advertising,

06:15

they don't need to spend as much money analyzing risk, and they don't need to spend as much

06:19

time talking to businesses only to find out half way through the process that that business

06:23

doesn't qualify for the loan. That's a LOT of friction taken out of the process on both

06:28

sides and both sides should want to pay for that service. And guess what; they do want

06:35

to pay for that service. In 2018, Peak Fintech helped with over 2500 transactions and had

06:41

less than 2% percent of those loans default. In 2019, they expanded to 2 other cities and

06:46

7 exed their revenue, from $1.6 million dollars to $11.7 million dollars, and in 2020 they

06:53

acquired the Jinxiaoer loan brokerage platform, expanding their footprint to 40 thousand loan

06:58

sales reps over 31 cities, and more than tripled their annual revenue again to $42.7 million

07:06

dollars. These physical financial centers help them collaborate with the cities they're

07:10

in and foster lending activities with lenders, businesses, and government officials that

07:15

want that face-to-face interaction. But didn't I just say that physical bank branches are

07:20

bad? In my opinion, that's true here in the US but there's no one-size-fits-all banking

07:25

solution for the whole world; face-to-face interaction is an important part winning the

07:30

ability to do business from the Chinese government and city officials, not just doing business

07:36

once you've approved. It's a different system there and Peak Fintech feels they need that

07:41

physical footprint to expand their reach today, in a digital world. Peak Fintech is expanding

07:47

their reach in a few ways. The first is by partnering other service providers to help

07:52

expand the list of things they can help small businesses do. This includes partnerships

07:57

with massive distributors that work with Chinese retail giants like JD.com, which is in ARKF

08:02

and ARKQ today. These distributors have access to hundreds of thousands of stores and retail

08:08

clients. They also have a business unit that focuses on payment processing to help facilitate

08:13

the actual financial transactions between these lendors and vendors, including much

08:18

sought-after services like cash advances. Peak Fintech is also expanding to adjacent

08:23

markets, like social media influencers, which are a popular and powerful marketing tool

08:28

in the Southeast Asia region. Remember my video on Sea Limited, when I talked about

08:32

Shopee's international expansion and the importance of understanding local markets and cultures?

08:43

[JACKIE CHAN] You're welcome.

08:48

Well, Gruppo Coin, Italy's largest department store chain, has thousands of these influencers

08:54

and Peak Fintech is willing and able to treat them as small business and help them secure

08:58

short-term loans. Overall, Peak's path to growth involves opening more financial centers

09:03

in more cities, partnering with more logistics solutions to help businesses with their supply-chains,

09:09

getting in the door with more of China's biggest retailers, and of course, eventually expanding

09:14

overseas. If we zoom back out, we can see that Peak Fintech is trying to be the connective

09:18

tissue between businesses, service providers, and financial institutions and charges a fee

09:24

for every transaction inside their ecosystem. When it matches a lender and a vendor, it

09:28

charges a service fee on the transaction. When businesses use Peak's platform to procure

09:30

products and their other supply chain services, there are service fees at various parts of

09:33

that value chain, and so on. It has 6 business units in total that all take service fees

09:36

based on what they're providing and to whom. These service fees range from one to four

09:41

percent, depending on the size and type of the transaction. That's the business model,

09:46

but before I talk about the financials, let me point out a few things about the STOCK.

09:50

First, Peak Fintech is actually a Canadian company and the operations of those six business

09:51

units are actually handled through their Chinese subsidiaries. This stock is not an ADR, so

09:52

these are direct shares there's no concern of de-listings, unlike stocks like Alibaba

09:58

and Nio. Second, its focus on small and medium sized businesses is in alignment with where

10:03

the Chinese government wants to see growth in production and employment. Peak Fintech

10:08

is helping the little guy, not the tech giants. Third, because Peak Fintech is business to

10:13

business, they're not dealing with sensitive consumer data directly, which is what a lot

10:18

of the regulatory crackdowns were focusing on. Consumers cannot provide funds on the

10:21

platform as with Lending Club or Prosper; all the lenders are banks or financial institutions.

10:23

So, in my opinion, a lot of the Chinese regulatory risks and concerns about future de-listings

10:27

don't apply to Peak Fintech. Here's a Zacks Research report published a couple weeks ago,

10:32

which does a great job aggregating and organizing all of Peak's most recent financials. Since

10:36

this isn't a first-party source, I went ahead and checked all the actuals against previous

10:37

Peak Fintech reports and they all match up, for example, the 11.7 million dollars of annual

10:38

revenue in 2019 versus the 42.7 million in 2020 that I showed you earlier. At the start

10:39

of September, Peak Fintech was trading on the OTC Markets under the ticker symbol PKKFF

10:43

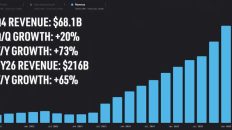

but is now on the NASDAQ as TNT. As you can see, Peak Fintech is roughly tripling their

10:49

revenues year over year, pretty much regardless of what quarter you look at. I also want to

10:54

point out that institutions don't hold this company yet. I'm not a financial advisor and

11:00

this is still a very young company, but in my opinion, this is an opportunity to get

11:05

out in front of the big guys and ride the wave when they drive the price up. And, like

11:09

I said earlier, this would be a perfect fit for Cathie Wood to hold in ARKF, so maybe

11:15

one of those institutions could even be ARK Invest.

11:18

The thing I really like about this Zacks report is that it tries to fill in the gaps. Given

11:22

the lack of China-based fintech platforms, they use the US and Canadian names they think

11:27

are comparable. They look at the enterprise value to sales ratio of these companies, take

11:32

out the highest and lowest companies, then calculate the average ratio for the rest.

11:36

I think this enterprise value to sales ratio is a fair way to value companies that are

11:40

still in growth mode. Zacks estimates Peaks 2021 sales will be around $96 million dollars

11:47

and their enterprise value at just over 1.4 billion dollars. If you give peak an EV to

11:53

sales multiple of 14.9, which is this average, you get $13 dollars per share. It's currently

11:59

trading at under $10, so that's a 30% percent upside. If you go by Peak Fintech's 2022 sales

12:04

estimates at an 11.6 EV to sales multiple, the stock could be $32 dollars per share next

12:11

year, representing a 3X opportunity from the ten dollars it is today. One thing I always

12:17

like to do is consider what happens if the company greatly under-performs. Let's say

12:22

they only get two thirds of the sales they expect in 2022, so $160 million instead of

12:28

238 million. That's still a share price of over 21 dollars using these same multiples,

12:35

so over a 2X in a year and and around $10 dollars today, instead of $13. There are obviously

12:41

a ton of financial metrics we can look at, but when it comes to hyper-growth companies,

12:45

I find that financials can change really quickly from quarter to quarter, especially if there's

12:50

a big acquisition, which I always harp on when I cover earnings. The one other metric

12:55

I'll point out here is the ratio of assets to liabilities. We want to make sure they're

13:00

not taking on too much bad debt in order to grow. They currently have about 61 million

13:05

dollars in assets and about 31 million dollars in liabilities, so a healthy asset-to-debt

13:10

ratio of about 2 to 1. However, that ratio was at 2.35 last quarter, so it did shrink

13:17

quite a bit and we should keep looking at it over time to make sure they're not taking

13:21

on too much debt compared to their assets. I think their financials are sound but I'll

13:27

include a link directly to Peak Fintech's investor presentation, as well as this Zacks

13:30

report on Peak Fintech in the description below so you can check out all of their financial

13:35

information for yourself; both documents are fairly short and do a great job summarizing

13:36

what the company does, how they do it, and whatever financial metrics you personally

13:37

look at for these volatile, high-growth companies.

13:38

Comment below or tweet me at ticker symbol YOU with your thoughts on Peak Fintech, ticker

13:41

symbol T N T. Do you think that T N T could end up in ARKF one day or do you think I'm

13:46

missing something big? Do you invest in companies overseas or stick to companies that operate

13:51

in your local markets? Is the explosive growth of this company exciting to you or do you

13:56

think it's too soon to tell? I'm excited to hear your thoughts, because as of right now,

14:00

I plan on buying TNT again in my $100,000 dollar portfolio, which I'll be opening if

14:06

and when Ticker Symbol: YOU hits 100,000 subscribers. The goal of that portfolio is to use all the

14:12

research and data I've been going over since I've started this channel to show how I would

14:17

grow an account starting from a clean slate, knowing what I know today. Just like some

14:22

investors compare their performance to the S&P500, I'll be comparing mine to ARKK, ARK

14:27

Invest's flagship innovation fund, over a 5 year time horizon — or until I have to

14:32

admit defeat. Either way, the goal is to provide a fun and interactive investing experience

14:37

for my awesome community. If you want to learn more about that project or the other holdings

14:41

in my personal accounts, check out my portfolio reveal episode, where I share pretty much

14:47

every investment I've made since I started the channel – no fluff, just data. I'll leave

14:51

a link to it in the top right hand corner of your screen right now and in the description

14:56

below as well. I think you'll really enjoy it. Until next time, this is ticker symbol

15:01

you. My name is Alex, reminding you that the best investment you can make… is in you.

If you want to comment on this, please do so on the YouTube Video Here