If you put $10,000 in Micron one year ago, you'd have almost $40,000 today. And if you drop that money into SanDisk, you'd have over $100,000 right now. That's because these companies are solving big bottlenecks in the AI market. So data centers are buying everything they make. And in this post, I'll highlight three more AI stocks winning big for the same reason, making them a great way to get rich without getting lucky. Your time is valuable, So, let's get right into it. First things first, I'm not here to hold you hostage. This video is all about optical networking, and here are the stocks I'm going to cover. Lumentum, ticker symbol LITE, which is the leading supplier of lasers and optical switches for AI data centers.

Coherent, ticker symbol COHR, which builds high-speed transceivers and optical interconnects.

And Sienna, ticker symbol C-I-E-N, which builds long-haul optical networks connecting multiple data centers together and of course which of these three stocks I think is the best buy right now.

I want to make the best use of your time, so let's start with the big picture and cover what these companies have in common like their markets, their revenues, and their risks right now.

Table of Contents

1. AI Bottlenecks

2. Turboquant Breakthrough

3. Optical Networking

4. Lumentum

5. Coherent

6. Ciena

7. Best Investment

8. Key Takeaways

AI Bottlenecks

AI data centers have three big bottlenecks: compute, memory, and networking, they're also limited by power, so every watt of compute, memory, and networking matters even more.

Gpus used to be the main constraint, but with each new generation, like Nvidia's Hopper, Blackwell, and Rubin, we have more compute capacity than most models actually need, so the real limit becomes how fast those gpus can access data and how quickly that data can be moved.

That's why I spend so much time covering companies like Micron, Broadcom, and Arista Networks, and why they've all outperformed the market.

Turboquant Breakthrough

But something big just happened in this space, which is why I'm making this video right now: Google Deepmind just released a data compression method called Turboquant, which optimizes how data is stored, retrieved, and reused by gpus.

Without getting too into the weeds, every time an AI model generates a token, it has to store lots of numbers in what's called the KV cache, for models with billions of parameters and long context windows, that KV cache can eat up most of a gpu's memory.

Turboquant is a huge deal because it cuts the KV cache size by over 80 percent, it speeds up key parts of inference by up to 8x, and it can be applied to existing models without any retraining or fine tuning.

This is a big breakthrough that will affect many parts of the AI stack, but here's the part we care about right now: thanks to Turboquant, gpus will spend a lot less time waiting on high bandwidth memory, which means they can process a lot more tokens in the same amount of time, as long as the network can keep up.

That means the network just became the next big bottleneck, so optical networking just became even more important.

Optical Networking

At a high level, optical networking is just networking with light instead of electricity, traditional routers and switches send electrical signals over copper wire, which works well for short distances, but breaks down for large distributed AI data centers.

Optical networks transmit light through glass fibers, which can carry much more data over much longer distances with much lower losses and interference, so while copper is great inside a server or inside one rack, serious AI clusters need optics to move data between racks, between buildings, and even across continents using undersea fiber optical links can push 400G, 800G, or even 1.6T of bandwidth per port.

G stands for Gigabits per second. Your copper internet connection at home is probably hundreds of megabits to 1 gigabit per second. If you google internet speed test, you'll see your current internet speeds, and hopefully they're close to what you're paying for. 1 gigabit per second is fast enough to stream dozens of 4k videos at a time a 400g optical connection in a data center is 400 times faster than that and 1.6 t means 1.6 terabits per second or 1600 g that's the kind of bandwidth that large ai clusters need as gpus start pumping out more tokens every second one more important point before we get into the stocks optical networking isn't a single product it's a full stack tiny laser chips and photonic components generate and detect the light.

Transceivers are the little plug-in modules that sit in a switch or in a server port to both transmit and receive data, which is why they're called transceivers. They turn electrical signals from the chip into light at one end of the fiber, and then they turn that light back into electrical signals at the other end. Then, full optical systems and software stitch all those links together into complete networks. Lumentum, Coherent, and Sienna dominate different layers of this stack making them great ways to invest in the shift to optical now that networking is becoming the next major bottleneck for AI But while everyone focused on AI and chip stocks gold has quietly rallied by 50 in the last year alone.

This is not financial advice and I'm not a licensed financial advisor, so do your own due diligence before making any investment decision, investing in mining stocks involves significant risk, including the possible loss of your entire investment, so make sure to see the full disclosure in the description below.

All right, Lumentum, Coherent, and Sienna all sell into the same core markets, hyperscale cloud providers, building AI clusters, big telecom operators upgrading their infrastructure, and large enterprises that need high capacity connectivity that ties their revenues directly to the same capex cycle that drives Nvidia, Broadcom, and the rest of the data center stack.

They also have similar business models, heavy upfront investments in research, fabs, and specialized manufacturing that turn into multi-year design wins and supply agreements for lasers, modules, and end-to-end systems, that means their margins depend on how fast hyperscalers and telecom carriers are expanding, since the more they sell, the more revenue they make against these big upfront fixed costs.

They also have similar risks, like customer concentration, a handful of cloud providers and telecom companies account for a big chunk of this market, so any pauses on spending can hit all three of these companies at once.

They also sit in the middle of complicated global supply chains for things like wafers, lasers, and advanced packaging; therefore, supply chain disruptions, export controls, or tariffs can impact costs and delay delivery timelines. And they all have serious competition from tech giants like Broadcom, Nokia, and Huawei, which limit their long-term pricing power once supply catches up with demand. But on the flip side, they also have the same big tailwinds ai optics alone are projected to jump from roughly an 18 billion dollar market in 2025 to around 90 billion dollars by 2030 and every time companies like nvidia and google solve a compute or memory bottleneck they put more pressure onto the network lumentum coherent and sienna are all positioned to capture revenue by releasing that pressure let's start with lumentum ticker symbol lite because they're currently the leader in lasers and optical switches for data centers.

Lumentum

Lumentum's latest quarter really tells the story here. Their revenue came in at $665 million, which is up 65% year over year. Their non-gap operating margins came in at 25.2%, up from just 8.2% a year ago. Most of that growth came from their components segment, which sells the laser chips and photonic parts that go inside high-speed transceivers and co-packaged optics modules for hyperscalers when you hear the term co-packaged optics that just means that the optical engines which are the parts with the lasers that turn electric signals into light and light back to electric again sit right next to the chip instead of at the edge of the circuit board today most switches use pluggable transceivers in the front panel which means every bit of data moves as electrical signals for several centimeters before getting converted into light at 800 or even 1600 G speeds that burns a lot of power and adds a lot of losses.

But co-packaged optics put the lasers in the same package as the switch chip or the accelerator, which makes the electrical distance a few millimeters. That 10x reduction in distance cuts power per bit by 30 to 70 percent It improves signal strength and it lets hyperscalers keep scaling to 1 or even 3 terabit per second speeds without melting their chips or their cooling budgets. That's why massive AI clusters are shifting more of their networks to optics, and Lumentum's ultra-high power lasers and optical engines are being built specifically for these deployments. So, if co-packaged optics are the future of AI networks, then Lumentum is the company selling the light. Lumentum's revenue from components hit $444 million last quarter, representing about two-thirds of their total sales.

And management is now guiding for around $805 million in total revenues for next quarter, which would imply 21% growth quarter over quarter. At OFC 2026, which is the Optical Fiber Communication Conference held earlier this month, Lumentum's management laid out a path to $2 billion in quarterly revenues within the next two years, roughly a 3x from here. That number is backed by real orders. The backlog for their R300 optical circuit switch is now over $400 million, and they're already booking massive orders for co-packaged optics shipments starting in 2027.

And of course, NVIDIA announced a multi-year agreement with Lumentum earlier this month, including a two billion dollar cash investment and a multi-billion dollar purchase agreement for lasers and optical engines.

NVIDIA gets priority access to future capacity for optics and Lumentum gets the funding and demand visibility to build out a new US fab in North Carolina to support up to five billion dollars in revenue capacity once it's fully ramped up.

For investors, the takeaway is simple: Lumentum is becoming a core part of NVIDIA's plan to scale AI factories, revenues and margins are growing fast, their backlog points to multi-year growth, and NVIDIA's 2 billion dollar investment and purchase commitments help lower their overall risk.

Coherent

If networking really is the next bottleneck for AI, then Lumentum is one of the few companies positioned to solve it, especially with NVIDIA in their corner.

All right, let's cover Coherent next, ticker symbol COHR, Coherent reported 1.7 billion dollars in revenue last quarter, that's up 17% year over year, with non-GAAP gross margins of roughly 39% and non-GAAP earnings per share of a dollar and 29 cents, that's up roughly 35% from a year ago.

That growth comes from their data center and communication segment, which generated about 1.2 billion dollars in revenue for the quarter, that's up 34% year over year, and now makes up over 70% of their total revenues, while their legacy industrial segment stayed roughly flat.

That shift from industrial to AI matters because of how Coherent makes their money. Unlike Lumentum, which focuses mostly on components, Coherent is vertically integrated across the whole Photonics stack.

They design and manufacture their own laser chips, package them into optical engines, and build complete 800G and 1.6t transceivers and other systems around them on their latest earnings call coherence management team said that most of 2026 is effectively booked with orders extending into 2027 and for every dollar of optics they delivered they booked over four dollars of new demand that's a very clear signal that demand is far ahead of supply given coherent a very healthy revenue backlog to work through.

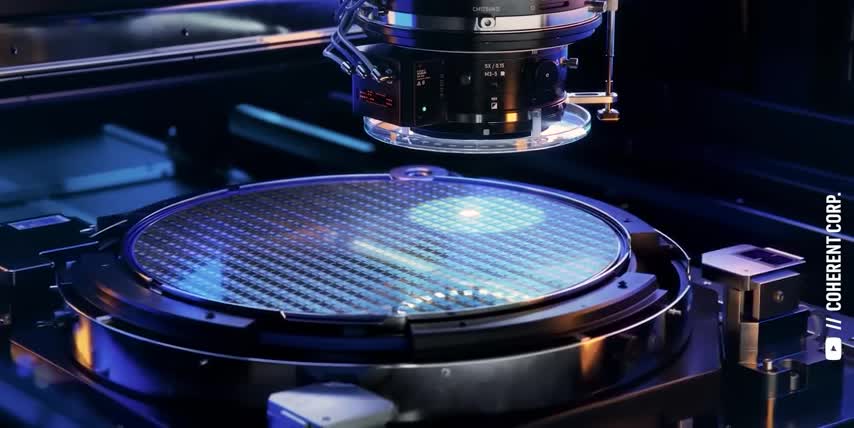

But a big part of coherence competitive edge is their six inch indium phosphide wafer fabs let me break that down for you silicon is great for compute but it's terrible for making light indium phosphide or inp is great for making and detecting the laser light used in fiber optic networks so it's the go-to semiconductor for lasers in optical transceivers modulators that encode that data onto light and photo detectors that convert it back to electrical signals on the other end.

Moving from three inch to six inch wafers let's coherent make more than four times the chips per wafer while cutting die costs by over 60 percent that's a massive cost capacity and margin advantage in a supply constrained market at ofc 2026 that same conference coherent showed off their 1.6 terabit transceivers they showed off advanced optical engines and end-to-end optical systems all built on this six inch inp process.

And just like with lumentum nvidia signed a multi-year strategic partnership with coherent including a 2 billion dollar investment and a multi-billion dollar purchase commitment for advanced lasers and optical networking products as an investor i really like coherence full stack approach to optics while lumentum is leaning into lasers optical engines and switches coherent is building the entire chain from their six inch wafers all the way to high speed transceivers.

Their revenues and margins are expanding thanks to explosive demand from AI data centers while Nvidia billion investment plus their purchase commitments lower the risk of all that upfront spending to ramp up production capacity over the next few years.

Ciena

Talk about a great way to get rich without getting lucky. And that leaves us with Ciena, ticker symbol Cien. Ciena sits one layer above coherent and lumentum turning all of those advanced optics into full ai networks sienna just had a record quarter over 1.4 billion dollars in revenue which is up roughly 33 year over year and their adjusted earnings per share more than doubled from a year ago they ended the quarter with a 7 billion dollar backlog which grew by 2 billion dollars in just the last three months but what's really changing for Sienna is their customer mix.

Revenue from cloud providers grew by 76% year-over-year, and now represents roughly 40% of their total revenue, a big shift from their traditional telecom carrier base to hyperscalers that are buying optical systems and data center interconnects. Sienna specializes in high-end optical signaling to squeeze more data into each fiber over longer distances. For example, their WaveLogic 6 is the industry's first 1.6TB per second solution that runs over a single wavelength. That lets operators double capacity on existing fibers while cutting power per bit, which effectively gives more power back to the GPUs. They're also working on AI-ready networks for Neo scalers, which are AI and cloud companies that want simpler, higher-capacity networks that use less space, less power, and less cooling.

The goal here is to automate more network operations, keep latency low, and utilization high across AI clusters that span multiple data centers. As an investor, I think of Sienna as the systems in silicon that sits one layer above coherent and lumentum. Those companies sell the lasers, the engines, and the transceivers, while Sienna packages them into full networks, so they win no matter which laser company comes out on top. And now that we have all that context, we can answer the big question. Which optical networking company is the best investment right now. And if you feel I've earned it, consider hitting the like button, subscribing to the channel, and sharing this video. That really helps me out, and it lets me know to make more content like this.

Best Investment

Thanks, now let's talk about Lumentum, Coherent, and Sienna stock. I think Lumentum is the most focused way to play the component side of AI Optics. They're doing $665 million in quarterly revenue they're growing 66 year over year with 42 gross margins and 25 operating margins while guiding to even higher margins over time on top of that they're building the lasers the optical engines and the switches that are already designed into next gen ai networks and they have nvidia as a strategic partner that de-risks a lot of that roadmap so if you want exposure to ai optical demand without paying for full systems, Lumentum is for you. Coherent is all about vertical integration.

They own the 6-inch Indium Phosphide Wafer Fabs, design their own laser chips, and ship complete 800G and 1.6T transceivers. Their data center revenue is growing fast, their data center backlog is growing four times faster than their shipments, and they have a multi-billion dollar investment and purchase agreement with NVIDIA. So if you're the kind of investor that looks for vertically integrated companies, that are also funded by NVIDIA, Coherent could be for you. Sienna sits one layer higher, turning lasers and optical engines into full networks that stitch AI data centers together. They just printed $1.4 billion in revenue, which is up 33% year over year.

They have adjusted gross margins in the mid-40s and a $7 billion backlog that gives them better revenue visibility than most hardware companies can dream of. With cloud and hyperscaler customers now driving a big chunk of their business, Sienna makes sense for investors who want a more diversified, systems-level way to play the optical networking build-out. Personally, I'd be happy owning all three, since that would give me broad exposure to the whole industry, from the laser chips and the engines, all the way up to the full AI networks. But if I had to pick a single winner, based on today's growth, backlog, positioning, and valuation, I'd pick coherent because I think their 6-inch wafer process plus Nvidia's investment give them the deepest moat and the best ratio of risk to reward.

I'm also a huge fan of vertical integration, but let me know which stock you're buying below. Or if you want me to make a deep dive video on any of these companies. And if you want to see more science behind the stocks, check out this post next. Either way, thanks for watching and until next time, this is ticker symbol U. My name is Alex reminding you that the best investment you can make is in you, and don't forget to follow TickerSymbol: YOU for more updates.

Key Takeaways:

- Lumentum, Coherent, and Sienna are three optical networking companies that are well-positioned to benefit from the growing demand for AI and cloud computing.

- Lumentum is a leader in lasers and optical switches for data centers, and has a strong partnership with NVIDIA.

- Coherent is a vertically integrated company that designs and manufactures its own laser chips and optical engines, and has a strong competitive edge due to its six-inch indium phosphide wafer fabs.

- Sienna is a systems-level company that packages lasers and optical engines into full networks, and has a strong backlog and revenue visibility.

- All three companies have similar business models and risks, but Coherent's vertical integration and NVIDIA's investment give it a unique advantage.

Checkout our YouTube Channel

Get the latest videos and industry deep dives as we check out the science behind the stocks.