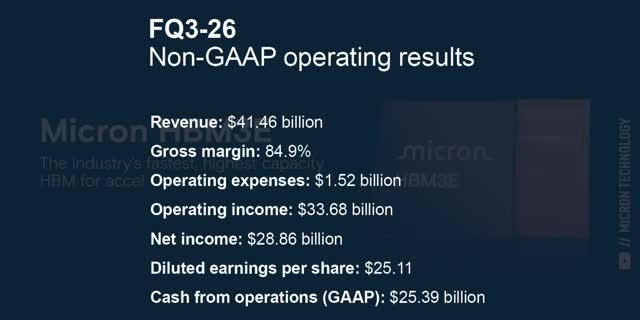

What if I told you that there's an AI tech giant hiding in plain sight? A company that builds the most critical components for the AI revolution, and it's even more profitable than NVIDIA. It's also growing faster and price cheaper than almost any other AI company, making this a great stock to get rich without getting lucky. Your time is valuable, so let's get right into it. You probably already know the name, and you might even own the stock, but there's a good chance that you're thinking about this company the wrong way. Just like most Wall Street analysts, last week, Micron reported the best quarter in their 48-year history. Revenue came in at $41.5 billion for the quarter, which is up by 74% quarter over quarter and 346% year over year.

Let me say that again, Micron's revenue almost doubled in the last 90 days, and it more than quadrupled over the last year. And their revenue guidance is $50 billion, which would imply revenue growth of 342% year-over-year for next quarter as well. Gross margins came in at 84.9%. That's not just higher than NVIDIA's, it's higher than most software companies like Meta Platforms. In fact, it's the highest gross margin that any physical chipmaker has ever publicly reported. When it comes to gross margins, Micron is the current king. I've been covering Micron for years now, and it's my second best performing stock of all time, only behind Nvidia. Here's what I think most Wall Street analysts have been missing this entire time. The margins and the revenues are not the story here.

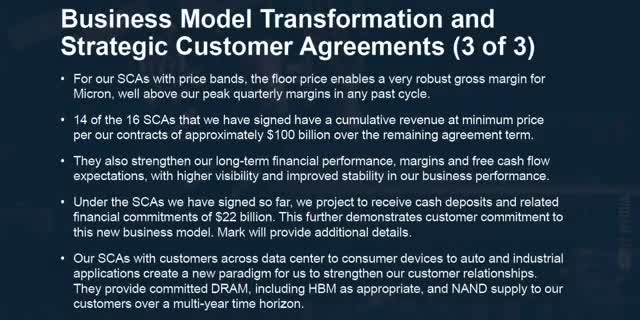

They're the proof that memory is no longer cyclical, and it's no longer a commodity. On this latest earnings call, Micron announced that they signed 16 strategic agreements with their largest customers, all of which run through 2030. These deals are structured so that customers either buy the chips that they committed to at the price they agreed, or they pay for the chips anyway. And to secure their spot in line, those customers paid Micron $18 billion before a single chip was shipped. So companies aren't just paying Micron for memory chips. They're paying to reserve the right to buy those chips in the first place years in advance. This is why it's so important to understand a company's products, not just their profits.

These contracts carry a combined minimum of roughly $100 billion in revenue at margins that are much higher than at any point in Micron's history. This is what I think the market hasn't priced in yet. Over the next five years, Micron is contractually guaranteed to earn their best margins ever. But before we can dive into these strategic contracts, we need to understand why the biggest AI companies on Earth are paying billions of dollars just to reserve Micron's memory in the first place, the science behind this stock. So let me show you why Micron is still one of the most undervalued AI companies on the market without all the industry jargon. The NVIDIA H100 is the chip that trained most of the AI models that we use today. It sits on a circuit board that's roughly the size of a textbook.

It uses 700 watts of power, which is about 7 light bulbs worth. And it can get so hot that the cooling hardware can weigh more than the chip itself. For years, Wall Street analysts focused on the GPU, the chip that does the number crunching and turned Nvidia into the most valuable company on the planet. But look at what surrounds it. Arranged in a tight cluster around the GPU are tiny towers of memory, each one smaller than a fingertip, and each one holding 16GB of memory built in a fundamentally different way than the sticks of RAM that we cram into our home computers This is high bandwidth memory or HBM and it matters more than almost anything else in the entire AI build Modern data centers don struggle to do the math behind AI.

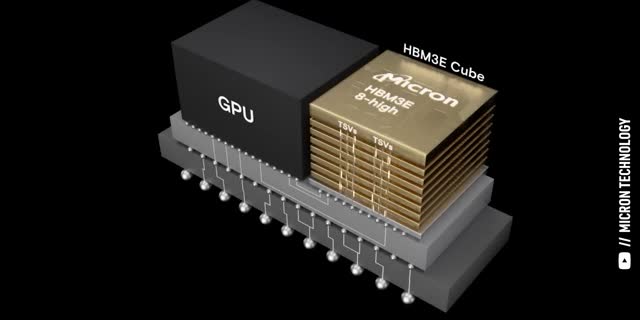

They have thousands of interconnected GPUs with thousands of compute cores each. The real struggle is feeding those GPUs data fast enough to keep them fully utilized. An idle GPU isn't just wasting time, it's burning money. Buying more GPUs doesn't solve this problem, it just makes the problem worse. So instead, data centers need memory that can feed every GPU as fast as those GPUs can crunch the numbers, which means the memory needs to have very high bandwidth. High bandwidth memory solves this exact problem by stacking memory vertically, 8-16 chips high, kind of like floors in a tiny skyscraper. Instead of the data traveling along a circuit board, it moves up and down this tower of chips, and the path it takes is 16 times wider than the memory we put in our PCs.

If HBM is a tower of chips, then the copper columns connecting them are like high-speed elevators. Each column is narrower than a single human hair, and there are thousands of them carrying data from each chip in the tower in parallel. As a result, one H100 can move over 3 terabytes of data every second. Or, said in English, that's fast enough to move around 600 full-length movies between chips every single second. At a high level, that's the science. Now, let's get back to the stock. High bandwidth memory isn't just another component on Nvidia's newest Blackwell chips. It's almost half the total manufacturing cost. Memory's share of the total manufacturing cost climbed from about 20% of the Nvidia Ampere A100s to roughly 45% of the Blackwell B200s today.

That's why I keep saying that memory is no longer cyclical, and it's not a commodity. It's one of the most valuable parts of the entire AI build-out, which is why Micron has become one of the most valuable companies on the entire market. But there's something else on the market that you need to know about, and that's your private data. There are hundreds of online data brokers making big money by collecting and selling your personal information. DeleteMe is a hands-free subscription service that will remove your personal information from those online data brokers.

They give you a quarterly privacy report showing everything they've done, and they've reviewed almost 60,000 listings for me so far. But what really surprised me is that these data brokers had way more than just my private data. They had my wife's and my entire families too. That's another reason I really like DeleteMe. They have a family plan, so we can all have more control over our personal data. So, if you care about your data and your family's privacy, you can get 20% off any consumer plan with my code, Symbol20, by going to joindeleteme.com slash Symbol20, or with my link in the description. And a big thank you to DeleteMe and to you for supporting the channel. Alright, like I said at the start of the video, Micron just reported their best quarter ever.

Revenues are up 346% year over year. Non-GAAP gross margins came in at 85%, and they guided to $50 billion in revenue for next quarter. Under normal circumstances, a report like that would be the perfect time to sell this kind of stock, if memory was still cyclical. Then, this would definitely be near the top of the cycle for For most of Micron's history, they had close to zero contracted revenue. Every chip was sold based on the monthly or quarterly spot price just like any other commodity They had no customer commitments they never got paid up front and sales were never guaranteed If Micron forecasts for memory demand were wrong then they paid a hefty price.

Either they made more chips than they could sell, or they wouldn't make enough and drive down the returns of all the infrastructure they invested in. And forecasts are almost always wrong. But Micron just flipped the entire script. They just announced 16 strategic customer agreements that run through 2030. These are not ordinary supply deals. They're structured as take or pay, meaning customers either buy the chips that they committed to or they pay for those chips anyway. There's no cancel button. And these aren't small orders either. The companies signing these contracts are the hyperscalers, companies like the ones building data centers that run ChatGPT, Google Gemini, Microsoft Copilot, and Meta's AI infrastructure.

They are locking in their memory supply years in advance because they cannot afford not to have it, especially when their competition does. 14 of those contracts carry a combined revenue minimum of roughly $100 billion. And to lock in their place in line, those customers paid Micron a combined $18 billion up front. That cash is collateral. If a customer cancels, Micron keeps the money. But this isn't just Micron taking advantage of desperate customers. These contracts are a win-win situation. Micron gets a price floor, guaranteed revenues regardless of how the market shifts over time. But on the flip side, their customers get a price ceiling. They won't have to pay insane prices if the memory shortage keeps getting worse and supplies get even more constrained.

That's what makes these contracts a solid long-term business model. Both sides have a reason to sign. I also want to emphasize that the $100 billion is the floor price. It's the worst price that Micron will be paid no matter what happens in the market. That means more than just guaranteed revenues. It means guaranteed margins. Margins well above the peak quarterly margins from any of their previous cycles. And the market hasn't fully priced this in yet. For the last two decades, analysts that were covering Micron couldn't model next year's revenue with any confidence. The company had no backlog and spot prices changed every quarter, so financial models went obsolete every few months. That's why memory companies used to trade at a steep discount to the rest of the market.

But these contracts get rid of that uncertainty for a third of Micron's revenue, and a bigger proportion as time goes on, while Wall Street's models are still catching up. Micron just went from zero contracted revenue to a $100 billion backlog, with $18 billion already in the bank. Again, proving that high bandwidth memory is not a cyclical business. And now that understand the science behind this stock and why this latest earnings call was so important, let me tell you why I'm still buying it, even though it's already a 10-bagger. And if you feel I've earned it so far, consider hitting the like button and subscribing to the channel. That really helps me out and it lets me know to make more deep dives like this. Thanks, now let's talk about my investment thesis for Micron.

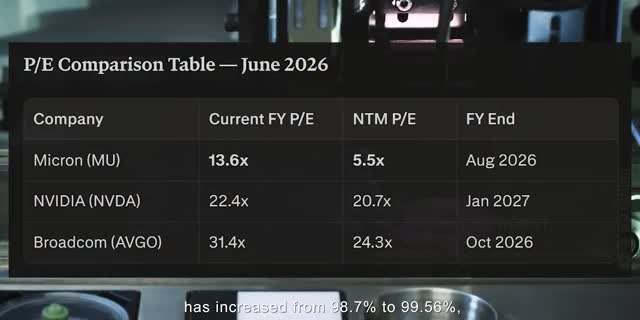

Micron currently trades at roughly 14 times their projected FY26 earnings. That number is 22.5 for Nvidia and 31.5 for Broadcom, meaning Micron trades at a decent discount relative to other trillion-dollar chip companies. And based on estimates for next year's earnings growth, Micron's forward P.E. ratio is just 5.5. That number is over 20 for both Nvidia and Broadcom, even though both companies are still growing fast. Let me say that again. Micron's earnings over the next 12 months are growing so much faster than their market cap that their forward price to earnings ratio is less than six even though they posting 346 revenue growth 85 gross margins and have a billion backlog In my opinion Micron is still so cheap because the market is still modeling it the old way.

This is honestly one of the strongest setups for long-term growth that I've seen in years. A $100 billion backlog, HBM supplies sold out through 2027, margin expansion from 39% to 85% in just a few quarters, and the stock is trading at under 6 times next year's earnings. The biggest risk to Micron is that all three major memory suppliers are expanding capacity at the same time. So if AI spending does slow down, supply could outpace demand. I personally don't see that happening with how much every hyperscaler is increasing their capex budget year over year. But even if it does, remember, Micron gets their $100 billion thanks to the take or pay structure of their strategic contracts, with $18 billion already in the bank. So Micron is positioned to get rich without getting lucky.

And so are Micron's shareholders. Let me point out one more thing because it's too important to leave out. Everything we've covered so far is the base case. It doesn't account for what could come next. The 16 strategic contracts cover about a third of Micron's current production, but they have four new fabs either under construction today or breaking ground right now. Every gigabyte of new capacity that Micron brings online is another contract waiting to be signed, not just by existing customers, but by others who already know the cost of being left behind. And while Wall Street analysts keep calling for AI spending to slow down, every single year, hyperscalers keep spending more. They're not cutting back. They're building data centers faster than everyone predicted.

And every one of those data centers needs more high bandwidth memory. There's also the demand side of the story. Every major breakthrough of the last 3 years has done the same thing. It's made AI cheaper to run, which makes more people use it for more use cases more often, which drives total compute demand even higher than before. So, the more efficient AI gets, the better an investment it becomes for those providing it. Which means memory demand will keep accelerating with the next big breakthrough. And the one after that. And the one after that. None of that is in today's models. None of that is in Micron's current 100 billion dollar backlog, and none of that is baked into their 4 P.E. ratio of just 5.5.

I've been covering Micron stock for years now, and this is the best setup I've seen for their long term growth. That's why I'm still dollar cost averaging into the stock before Wall Street finally catches on. And if you want to see more stocks that I'm buying to get rich without getting lucky, check out this post next.

Table of Contents

1. Introduction to Micron

2. The Science Behind Micron

3. Micron's Strategic Agreements

4. Investment Thesis for Micron

5. Key Takeaways

Introduction to Micron

Micron is a leading manufacturer of memory chips, including high bandwidth memory (HBM). The company has reported significant revenue growth and has signed strategic agreements with major customers.

The Science Behind Micron

Micron's HBM is used in data centers to feed GPUs with data. The memory is stacked vertically, 8-16 chips high, allowing for high bandwidth and low latency.

Micron's Strategic Agreements

Micron has signed 16 strategic agreements with major customers, including hyperscalers. These agreements provide a guaranteed revenue stream for Micron and help to reduce uncertainty.

Investment Thesis for Micron

Micron's strong financials, strategic agreements, and growing demand for HBM make it an attractive investment opportunity. The company's valuation is also relatively low compared to its peers.

Key Takeaways

Here are the key points to take away from this article:

- Micron is a leading manufacturer of memory chips, including HBM.

- The company has reported significant revenue growth and has signed strategic agreements with major customers.

- Micron's HBM is used in data centers to feed GPUs with data.

- The company's valuation is relatively low compared to its peers.

- Micron is an attractive investment opportunity due to its strong financials, strategic agreements, and growing demand for HBM.

Checkout our YouTube Channel

Get the latest videos and industry deep dives as we check out the science behind the stocks.